TL;DR:

- Corporate merchandise budget planning involves allocating funds by use case, product tiers, and logistics to maximize return on investment. It requires quarterly forecasting, total landed cost calculations, and strict approval controls to prevent overspending. Implementing governance and measuring ROI ensure programs are financially sustainable and valuable.

Corporate merchandise budget planning is the process of allocating financial resources across use cases, product tiers, and logistics to maximise return on investment and brand presence. Most organisations treat branded merchandise as a one-off purchase rather than an operating programme. That approach produces panic orders, undefendable spend, and wasted budget. A structured plan built on quarterly forecasting, tiered allocation, and finance-grade controls transforms merchandise from a cost line into a measurable brand asset. This guide gives corporate executives and budget managers a practical framework to do exactly that.

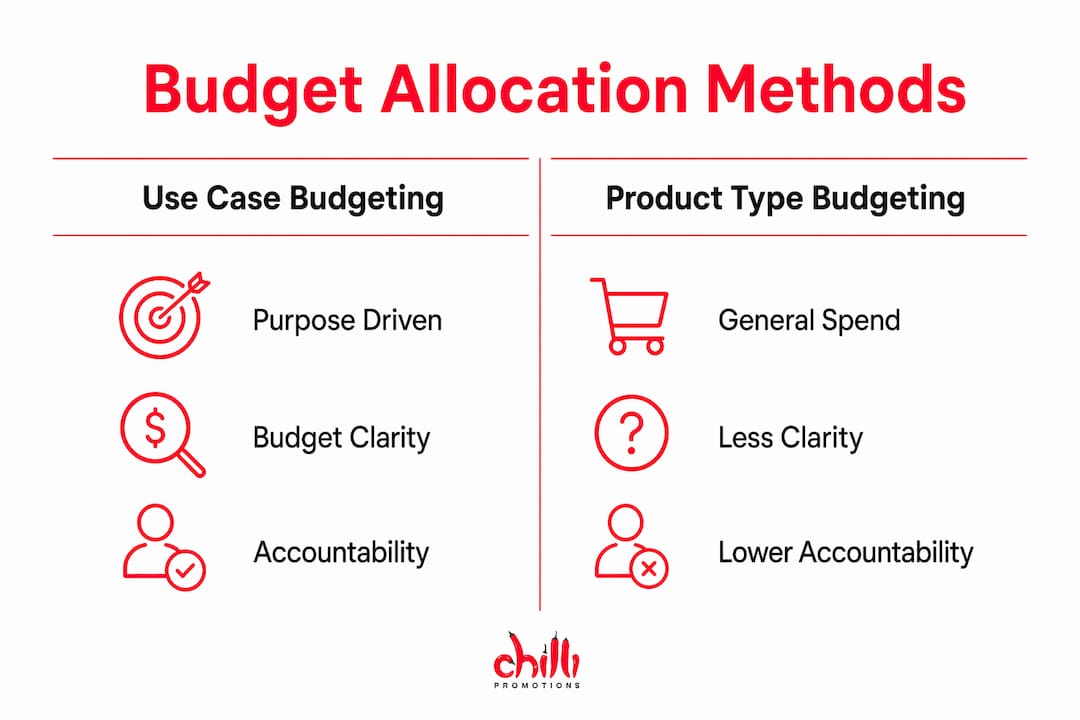

How to structure your corporate merchandise budget planning by use case and tier

Budgeting by use case rather than by product type is the single most effective shift you can make. When you organise spend around purposes such as client gifting, event activations, and employee onboarding, every dollar has a clear owner and a clear outcome. Product-based budgeting, by contrast, produces a catalogue of items with no clear connection to business goals.

Tiered budgeting adds a second layer of discipline. Each use case carries a different recipient value, so the spend per item should reflect that. Typical 2026 gifting tiers sit at $50–$100 for client thank-yous, $100–$250 for key clients, $250 and above for VIPs, and $50–$150 per gift for employees. These ranges give finance teams a defensible framework when approving spend requests.

Value drivers matter more than unit cost. Frequency of use, longevity, perceived value, relevance, and distribution context should guide tier selection, not just the price tag. A $30 item used daily for two years delivers far more brand value than a $60 item used once.

The table below compares the two main allocation methods.

| Allocation method | Basis for spend | Budget clarity | Accountability |

|---|---|---|---|

| Use case budgeting | Purpose and recipient type | High: each line tied to a goal | Clear owner per use case |

| Product-based budgeting | Item category or SKU | Low: spend disconnected from outcomes | Shared or unclear |

Pro Tip: Treat each use case as a mini programme with its own brief, recipient profile, and success metric. This makes budget reviews faster and approval conversations shorter.

Treating merchandise as an operating programme rather than a one-off purchase stabilises order patterns and makes annual budget submissions far easier to defend. Finance teams respond well to programmes with defined parameters. They push back on vague line items.

How to forecast your merchandise budget quarterly with logistics included

Quarterly forecasting works because merchandise demand follows discrete calendars. Hiring cycles, product launches, trade shows, and seasonal campaigns all cluster around predictable windows. Aligning your forecast to these milestones reduces rush orders and the cost spikes that come with them.

The most common forecasting error is budgeting only for the product cost. Total landed cost includes production, inbound freight, duties, customs brokerage, last-mile handling, and a returns reserve. Ignoring these cost layers underestimates true costs by 10–20%. That gap is large enough to blow a quarterly budget in a single campaign.

The table below shows the components of a landed cost calculation and their typical impact.

| Cost component | What it covers | Budget impact |

|---|---|---|

| Product cost | Unit price including decoration | Base figure |

| Inbound freight | Shipping from supplier to warehouse | Adds 8–15% on average |

| Duties and tariffs | Import charges where applicable | Variable by origin country |

| Customs brokerage | Clearance fees | Fixed cost per shipment |

| Last-mile handling | Delivery to recipient or event | Adds per-unit cost at scale |

| Returns reserve | Allowance for damaged or undelivered items | Typically 2–4% of order value |

Build a buffer of 3–5% on top of your total landed cost estimate. Unexpected expenses such as reprint requests, last-minute additions, or carrier surcharges are routine, not exceptional. A buffer prevents these from requiring a formal budget amendment.

Pro Tip: Lock in production windows at least 90 days before major campaigns. Suppliers offer better pricing and guaranteed capacity when lead times are respected. Waiting until 30 days out costs more and risks delays.

Accurate landed cost accounting is the foundation of meaningful forecasting. Without it, your quarterly numbers are optimistic fiction. With it, you can present finance with a credible, auditable plan.

What finance-grade budget controls look like for merchandise programmes

Finance-grade controls for merchandise programmes include per-user credit limits, department spending caps, approval routing, real-time spend dashboards, and order history reporting. Enterprise programmes commonly set approval thresholds at $150 or $250, with department caps such as $3,000 per quarter for Sales and $1,500 for Engineering. These numbers are not arbitrary. They reflect the typical order sizes and recipient volumes for each team.

Approval thresholds alone are not sufficient. Threshold approvals require explicit controls such as credit limits and spend caps to function as genuine governance rather than procedural checkboxes. Without those controls, a threshold only catches overspending after it has already occurred.

Pre-production approval routing solves this problem. When orders require sign-off before production begins, you prevent wasteful runs and inventory stagnation. After-the-fact approvals are common in poorly structured programmes and they create reconciliation headaches at quarter end.

Best practices for transparency and record-keeping include:

- Request tracker: A gift request tracker with approval-status visibility gives finance an audit-ready record of every order.

- Department cost attribution: Tag every order to a cost centre so spend rolls up correctly in monthly reports.

- Spend dashboards: Real-time visibility lets managers self-correct before hitting caps, rather than discovering overruns in the next finance review.

- Policy documentation: Written rules for who can approve what, at what threshold, and for which use cases remove ambiguity and reduce escalations.

These controls are not bureaucratic overhead. They are the difference between a merchandise programme that scales and one that gets cut at the next budget review.

How to measure and present the ROI of your merchandise spend

The standard ROI formula for merchandise programmes is: (Total Value Generated minus Total Programme Cost) divided by Total Programme Cost, multiplied by 100. Soft outcomes translate to finance by assigning monetary values to retention, engagement, onboarding efficiency, and brand amplification. Each of these has a calculable proxy. Reduced employee turnover has a known replacement cost. Earned media value from brand impressions has an established benchmark.

Cost-per-impression (CPI) is the most widely used benchmark for promotional item value. A $6 tote bag averages 1/10 of a cent CPI and a $13 baseball cap averages 3/10 of a cent. These figures reflect thousands of impressions generated over the lifespan of a single item. No digital ad format comes close to that cost efficiency at scale.

Practical steps for measuring merchandise ROI include:

- Set baseline metrics before the programme launches. Track employee retention rates, event engagement scores, and client renewal rates as pre-programme benchmarks.

- Assign a monetary value to each outcome. Use your HR team’s cost-per-hire figure for retention, and your marketing team’s CPM rate for brand impressions.

- Track on-demand ordering rates. On-demand platforms reduce overstock waste, which directly improves your cost-per-outcome figure.

- Report quarterly, not annually. Quarterly reporting catches underperforming use cases early and allows reallocation before the full budget is spent.

Boosting brand visibility through well-chosen merchandise is measurable when you build the tracking framework before you place the first order. Retroactive measurement is always incomplete. Prospective measurement is always more credible to finance.

Calculating marketing ROI with the same rigour applied to paid media gives merchandise programmes the financial credibility they need to survive budget cycles. Programmes that cannot show ROI get cut. Programmes that show clear returns get increased funding.

Key takeaways

Effective corporate merchandise budget planning requires structuring spend by use case and tier, forecasting total landed cost quarterly, and enforcing finance-grade controls before production begins.

| Point | Details |

|---|---|

| Budget by use case, not product | Tie every spend line to a purpose such as gifting, events, or onboarding for clear accountability. |

| Include full landed cost | Add freight, duties, handling, and a 3–5% buffer to avoid underestimating true costs by 10–20%. |

| Lock production windows early | Commit to suppliers 90 days before major campaigns to secure pricing and avoid rush premiums. |

| Apply pre-production approvals | Route orders for sign-off before production starts to prevent waste and reconciliation problems. |

| Measure ROI with baseline metrics | Set retention, engagement, and impression benchmarks before launch so ROI reporting is credible. |

The real challenge in merchandise budgeting is not the numbers

After more than two decades working with corporate clients across Australia and New Zealand, the Chilli Promotions team has seen the same pattern repeat itself. Organisations invest time building a detailed budget, then undermine it by skipping the governance layer. The spreadsheet looks right. The approvals process does not exist.

The uncomfortable truth is that most merchandise budget blowouts are not caused by expensive products. They are caused by late decisions, unclear ownership, and orders placed outside the approved programme. A $15 item ordered in a rush at three times the quantity needed costs more than a $40 item planned six months in advance.

The other pattern we see is organisations treating sustainability as a premium add-on rather than a budget consideration from the start. Sustainable promotional products often have comparable unit costs to conventional alternatives when ordered at the right volume and lead time. Waiting until the last minute removes that option entirely.

Our advice is to build the governance framework first and the product catalogue second. Define your use cases, set your tiers, establish your approval thresholds, and then select products that fit within those parameters. That sequence produces programmes that finance teams approve and recipients actually value.

— Chilli Promotions Team

How Chilli Promotions supports your merchandise budget

Chilli Promotions has partnered with corporate clients across Australia and New Zealand since 2001, helping teams translate budget frameworks into branded merchandise programmes that deliver real results.

Whether you are planning corporate giveaways for a product launch, building an employee onboarding kit, or sourcing event merchandise across multiple tiers, Chilli Promotions works as a vested partner in your programme. The team brings category knowledge, supplier relationships, and production planning expertise to every brief. Explore the full promotional products range or contact Chilli Promotions directly to discuss your 2026 merchandise programme.

FAQ

What is corporate merchandise budget planning?

Corporate merchandise budget planning is the process of allocating spend across use cases, product tiers, and logistics to maximise brand ROI. A structured plan includes quarterly forecasting, total landed cost accounting, and finance-grade approval controls.

How much should a company spend per corporate gift?

Typical 2026 tiers range from $50–$100 for client thank-yous, $100–$250 for key clients, $250 and above for VIPs, and $50–$150 per gift for employees. The right tier depends on recipient value and the use case objective.

What is total landed cost in merchandise budgeting?

Total landed cost includes the product price plus inbound freight, duties, customs brokerage, last-mile handling, and a returns reserve. Excluding these layers underestimates true costs by 10–20%, which is a common cause of quarterly budget overruns.

How do approval workflows prevent merchandise overspending?

Pre-production approval routing stops orders before they are placed, rather than flagging overruns after the fact. Effective controls combine per-user credit limits, department caps, and written policies that define who can approve what at each threshold.

How do you calculate ROI for a merchandise programme?

The formula is: (Total Value Generated minus Total Programme Cost) divided by Total Programme Cost, multiplied by 100. Assign monetary values to outcomes such as employee retention, onboarding efficiency, and brand impressions using your organisation’s existing cost benchmarks.